Non-manufacturing costs Strategic Cost Management Vocab, Definition, Explanations Fiveable

For example, a small business that manufactures widgets may have fixed monthly costs of $800 for its building and $100 for equipment maintenance. These expenses stay the same regardless of the level of production, so per-item costs are reduced if the business makes more widgets. Table 1.2 provides several examples of manufacturing costs at Custom Furniture Company by category. Fluctuation of costs is yet another challenge that makes it harder to calculate manufacturing costs accurately, according to Fabrizi. The next step is to calculate the costs of utilities (electricity, water, or gas) that are directly used in the manufacturing process (for example, fuel used to operate the production equipment). Next, calculate the value of the existing inventory if the manufacturing company already has a stock of materials from a previous period.

Production Costs vs. Manufacturing Costs Example

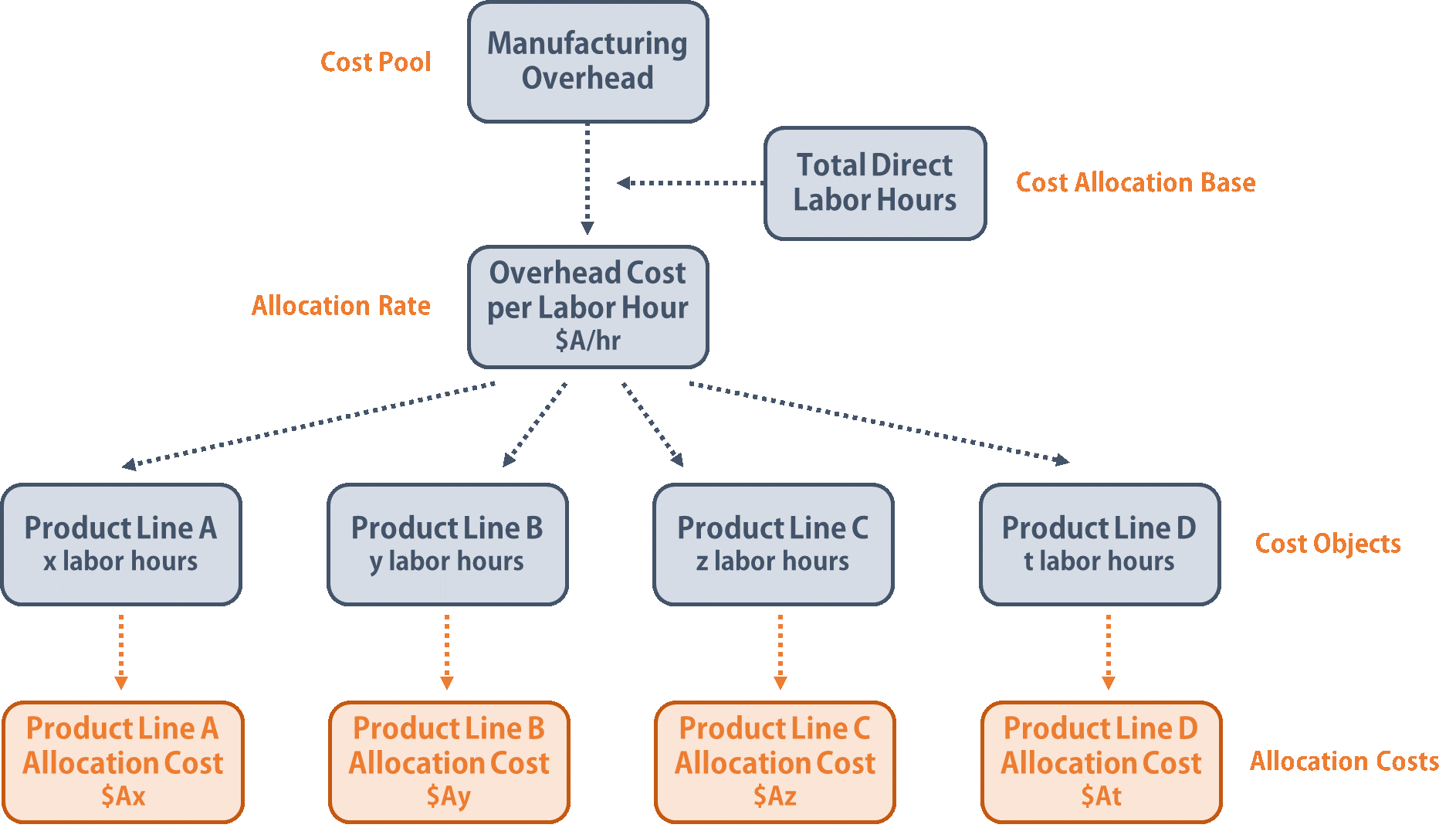

By calculating manufacturing costs, companies can clearly understand the true cost of making a product. Based on this information, the company’s management can add a markup to determine competitive selling prices for their products. Indirect manufacturing costs include all other expenses incurred in manufacturing a product except direct expenses. Variable costs – vary in total in proportion to changes in activity. Examples include direct materials, direct labor, and sales commission based on sales. Direct costs – those that can be traced directly to a particular object of costing such as a particular product, department, or branch.

Production Costs

Some operating expenses can also be classified as direct costs, such as advertising cost for a particular product. Recall from other tutorials that variable costs change in proportion to production. For instance, in our example of Friends Company, the company purchases metal parts (raw material) to produce valves. The more valves are produced, the more parts Friends Company has to acquire.

The Difference Between Manufacturing and Nonmanufacturing Costs

Manufacturing costs, also called product costs, are the expenses a company incurs in the process of manufacturing products. Costs that fluctuate based on the level of production or sales, such as raw materials and direct labor. Examples of general and administrative costs include salaries and bonuses of top executives and the costs accounting and finance mcq quiz with answers test 1 of administrative departments, including personnel, accounting, legal, and information technology. As a result, the company decided to outsource production to a contract manufacturing company (a company that enters into a contract with the manufacturer to make certain components) instead of assembling components in-house.

These costs are reported on a company’s income statement below the cost of goods sold, and are usually charged to expense as incurred. Since nonmanufacturing overhead costs are treated as period costs, they are not allocated to goods produced, as would be the case with factory overhead costs. Since they are not allocated to goods produced, these costs never appear in the cost of inventory on a firm’s balance sheet. Although selling costs and general and administrative costs are considered nonmanufacturing costs, managers often want to assign some of these costs to products for decision-making purposes. For example, sales commissions and shipping costs for a specific product could be assigned to the product.

- Identifying, separating and apportioning cost data provides management and outside decision makers (investors) valuable information on the company’s profitability and cost control systems.

- Manufacturing costs, for the most part, are sensitive to changes in production volume.

- That number is, of course, critical to setting the wholesale price of the item.

- A balance sheet is one of the financial statements that gives a view of the company’s financial position, while assets are the resources a company owns.

Figure 2.3.1 shows examples of production activities at Custom Furniture Company for each of the three categories. Figure 1.4 shows examples of production activities at Custom Furniture Company for each of the three categories (we continue using this company as an example in Chapter 2). Non-manufacturing costs include those costs that are not incurred in the production process but are incurred for other business activities of the entity. These costs do not specifically contribute to the actual production of goods but are essential to ensure overall functioning of the business.

Study finds a new way for next-generation biofuel production to finally become both cost-effective and carbon neutral. “When considering new technologies, such as biomass-based plastics, if we can account for the benefit of carbon storage in the material, we can make them more cost-effective in the market,” Van Roijen said. Kavitha Simha is a productivity author and researcher, passionate about finding smarter ways to manage time. Combining her knowledge of multiple disciplines, she seeks to help others optimize their work-life balance, which she believes is the key to minimizing stress.

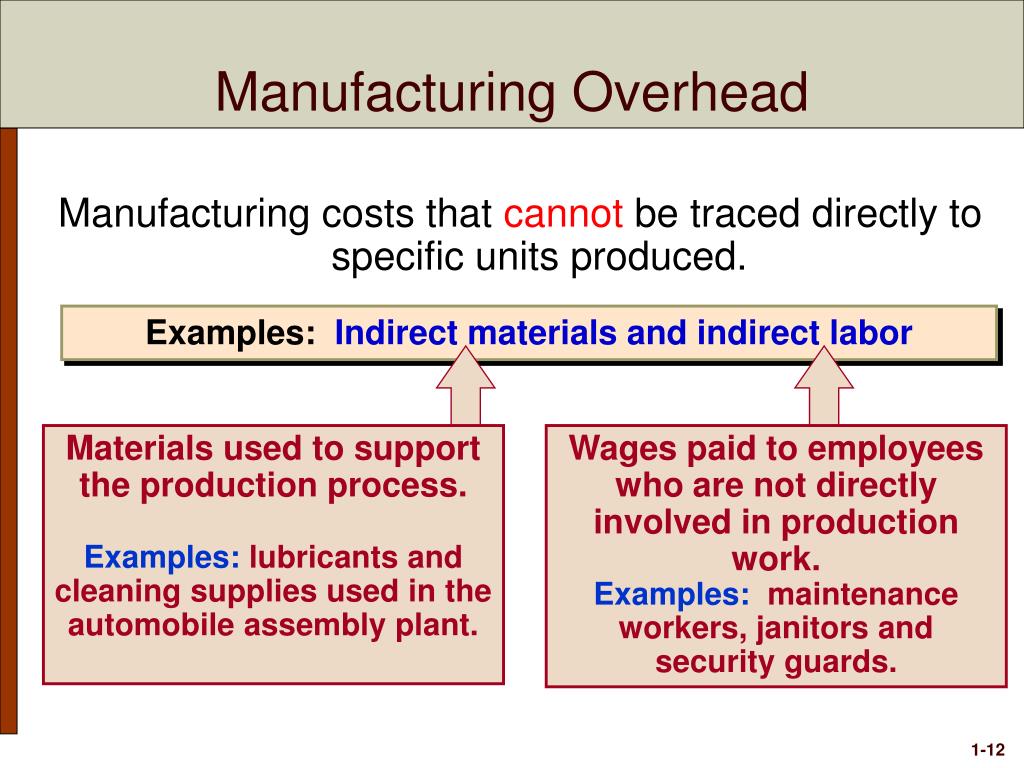

Manufacturing overhead includes the indirect materials and indirect labor mentioned previously. Other manufacturing overhead items are factory building rent, maintenance and depreciation for production equipment, factory utilities, and quality control testing. Since nonmanufacturing overhead costs are outside of the manufacturing function, these nonmanufacturing costs are immediately expensed in the accounting period in which they are incurred. That is why accountants refer to nonmanufacturing costs as period costs or period expenses. The wood used to build tables and the hardware used to attach table legs would be considered direct materials.

Nonmanufacturing overhead costs are the company’s selling, general and administrative (SG&A) expenses plus the company’s interest expense. In this example, the total production costs are $900 per month in fixed expenses plus $10 in variable expenses for each widget produced. To produce each widget, the business must purchase supplies at $10 each. After subtracting the manufacturing cost of $10, each widget makes $90 for the business. The company engaged a consulting firm to help them find out what factors were driving up manufacturing costs.